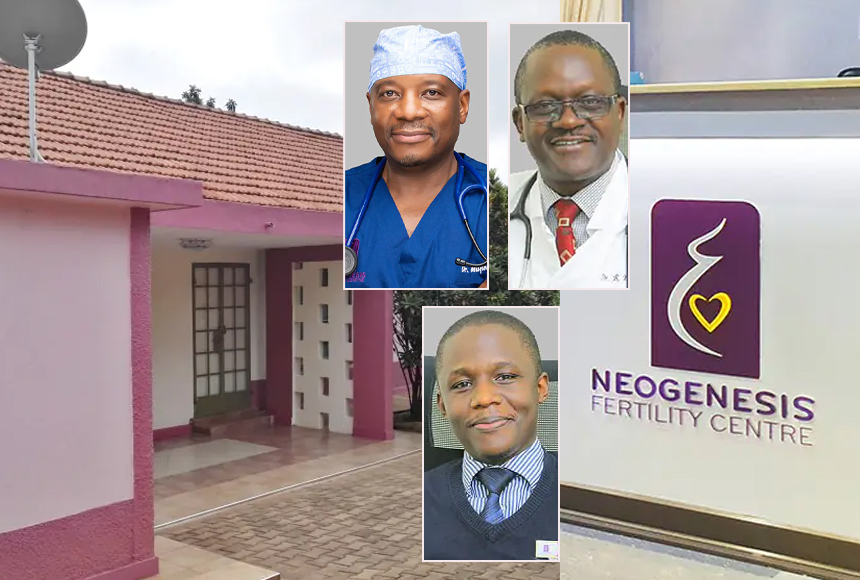

Daniel Nasasira the Assistant Registrar of Companies at Uganda Registrations Service Bureau (URSB) has issued tough orders to city medical doctors who are fighting over Bukoto based Neogenesis Fertility Centre Limited.

The orders resulted from a complaint filed by Dr Enock Mwanje against other company shareholders who include Dr. Mark Muyingo Tomusange, Dr. Robert Bazare Busingye, Dr Davis Rujumba who accused him of mismanaging the company finances and after sidelined him from the operations of the company which they as incorporated in 2017.

The Registrar agreed with the petitioner that he was denied his statutory and proprietary rights by being excluded from participation in the affairs of the Company, was restricted from accessing company information, and broader claims of oppressive conduct.

He further noted that the manner in which the Company’s affairs have been handled and the protection of the Petitioner’s rights as a member, which are matters falling squarely within the statutory jurisdiction of the Registrar under the Companies Act gives him the jurisdiction to preside over the complaint.

More Read

The Registrar stated that he was not satisfied with the respondent’s defence after they claimed that the petitioner absented himself from the running of the company noting that they didn’t provide any evidence showing that they issued a formal written notice when one of their fellow directors Dr Dennis Kinene was selling his 16% shares so that he also participates in the transaction.

“Accordingly, I find that the arbitration clause contained in Article 12 of the Company’s Articles of Association is not applicable or binding in respect of this Petition. The clause is restricted to disputes concerning valuation in voluntary share transfers in the ordinary course of business, whereas the present matter concerns allegations of oppression and infringement of participatory rights, which properly fall for determination by the Registrar of Companies,” the Registrar stated.

He further rubbished the respondent’s defence that the exclusion of the petitioner from participating in the company affairs was a fair dealing because he was frustrating the operations of the company noting that what they did amounts to an infringement of an aggrieved party’s participatory rights.

“The Petitioner’s exit from the Directors’ WhatsApp group in 2022 did not extinguish or waive his statutory and participatory rights to receive notice of, attend, and participate in company meetings,” he stated.

He further established that there is irretrievable breakdown in the relationship between the Petitioner and the Respondents which is characterised by loss of trust, breakdown in communication, and persistent disputes over the management and direction of the Company.

He added that in such circumstances, it would be impractical and contrary to the interests of the Company to compel the parties to continue in a strained corporate relationship. He thus directed that a buyout of the Petitioner’s shares would be the most equitable and commercially sensible remedy, as it brings finality to the dispute while allowing the Company to continue its operations without disruption.

He strongly encouraged parties to cooperate in good faith to bring to a closure their dispute and restore stability to the Company noting that the petitioner’s shares should be bought out at a fair value by the company itself or other shareholders jointly or severally.

He directed that a qualified and independent valuer be appointed within thirty-one days from the date of this ruling by mutual agreement of the parties, and in default of agreement by a competent Court, for purposes of determining the fair value of the Petitioner’s shareholding and contributions in the Company.

He advised that valuation shall be conducted in accordance with internationally accepted valuation principles and standards, taking into account the Petitioner’s shareholding, his capital contributions, historical participation, and any other relevant equitable considerations necessary to arrive at a fair and just valuation.

He further directed that the valuation report shall be completed and submitted to the parties within ninety days from the date of appointment of the independent valuer and upon receipt of the valuation report, the purchase price shall be paid to the Petitioner within one hundred eighty days, unless otherwise agreed by the parties in writing.

The registrar also directed that upon full payment of the purchase price, the Petitioner shall execute all necessary transfer instruments and documents to effect the transfer of his shares, and the Company shall update all statutory records accordingly.

He noted that as pending completion of the buy-out process, all parties shall maintain the status quo and shall refrain from any acts likely to prejudice the Company’s operations, assets, financing arrangements, employees, contractual obligations, or commercial reputation.

{kind=link}